The unwillingness of the majority elected by America into Congress and the Presidency to continue Pandemic-era subsidies for ObamaCare premiums means many lower middle class families will face a choice this Fall during Open Enrollment. You know Americans who’ve abandoned banks for credit unions. It’s time to do the same for health payment, but in this case upgrading from insurance to Sharing.

Will families be able to pay 75% more to avoid catastrophic, unexpected health expenses, or will they do some homework to learn about an insurance alternative that gives them such protection but without the expense?

Not only have the millions of Americans in Sharing plans escaped a huge expense, but also as newly-minted cash patients they no longer have to find a doctor in a network that notoriously excludes up to 40% of a local area’s providers (and those doctors in networks face pressure to conform to low-quality protocols, or risk getting booted from the network; do you want to be operated on by a doctor whose discretion is handcuffed when trying to give you the best advice?).

When a sickness or accident requires a specialist or medical treatment, Sharing members call our Concierge who have search programs to help patients access quality-priced drugs, tests, specialists & procedures - and every provider now has a cash price, usually heavily discounted.

Sharing patients (& their doctors) also won’t have to tolerate an adversarial process to get their claims paid. Over 20% of insurance claims are denied, sometimes using Artificial Intelligence. Sharing communities list what’s shareable in what are called “guidelines”, and if the service is listed, the bill gets shared by the community.

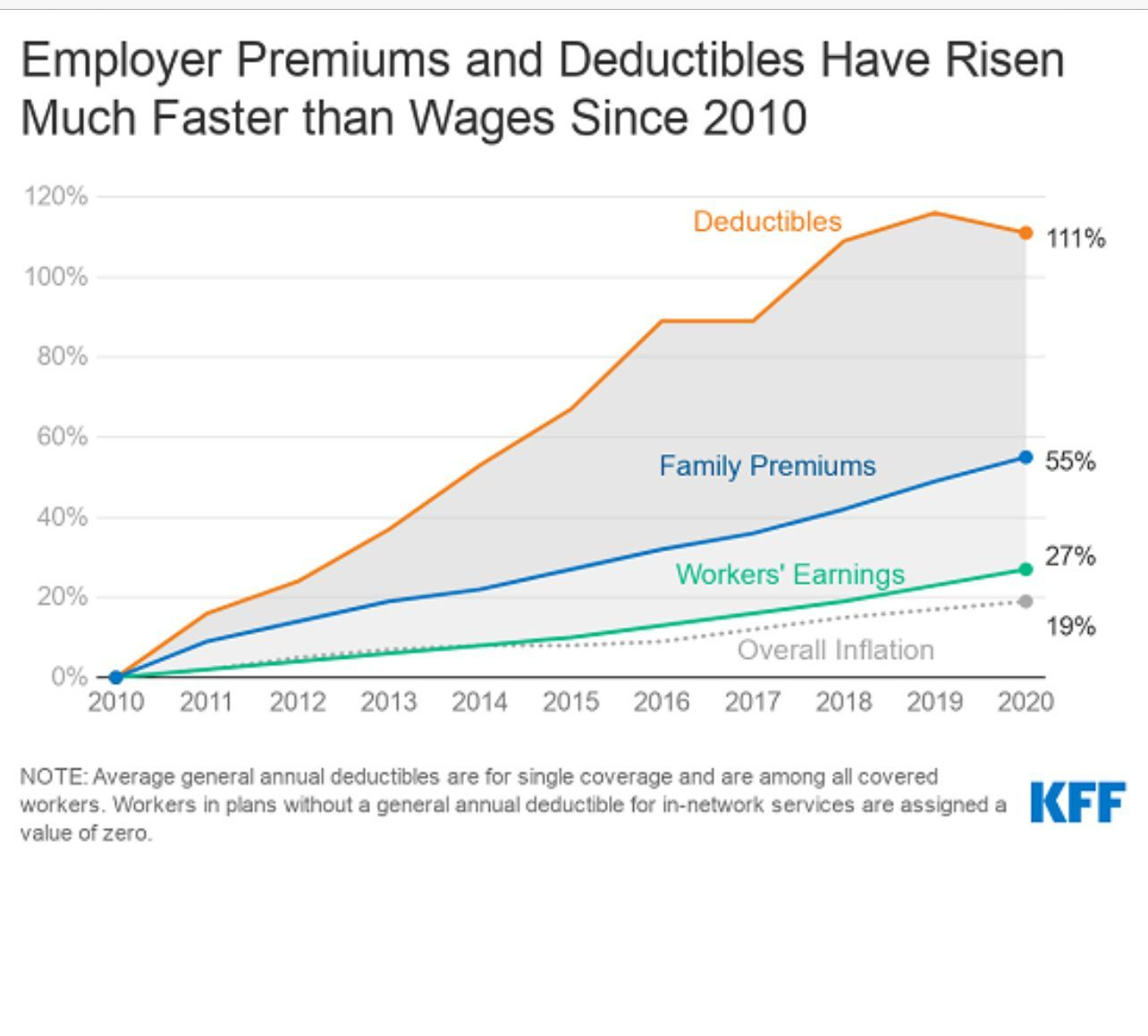

And now reports on loss of ObamaCare subsidies warn that cheaper policies to be offered will be cheap because they don’t kick in until the patient has paid $10,000 ($21K for a family!). That’s quite a high deductible, four thousand dollars higher than the current average. Sharing plans can have modestly high “deductibles”, what we call instead “Initial Unshareable Amounts” (IUAs), reaching $5K.

To listen to my healthplan discussion with pharmacist Needham, click here.

But Sharing plans can lower ones out of pocket liability for a sickness or accident to as little as $1,000 or even $500! (It cost more per month to do so, and I recommend the higher IUA and then combining Sharing with an Health Savings Account (HSA) to handle lower cost medical services. One needs discipline, of course, to properly fund the HSA so it’s ready for use when one suffers a medical expense.

Trump’s expanded, affordable, catastrophic plans (remember, with the $10,000 deductible!) won’t even be available in all 50 states.

From this source, “…insurers don’t offer (catastrophic) plans at all in 10 states: Alaska, Arkansas, Indiana, Louisiana, Mississippi, New Mexico, Oregon, Rhode Island, Utah, and Wyoming. And where they are available, options are few. This year, for example, a 25-year-old in Orlando, Florida, had a choice of 61 “bronze” plans, the cheapest level of coverage available to all ACA shoppers, but just three catastrophic plans.”

It’s time to watch my video, scrolling down here, then scrolling back up to fill out the “questionnaire”. Whether a head of household or CEO, your answers will be emailed to me, triggering my reaching out to schedule a discussion on your wants and needs - and our options that might help.

Our average $300/month charge will impress prospects, but they should ensure they’re healthy enough to enroll and not expect catastrophic events from any condition of theirs that preceded membership by the last couple years. Any American who suffered heart disease or cancer in the past should know that any new episode that can be connected to a pre-existing condition will trigger a phased-in sharing of such expenses.

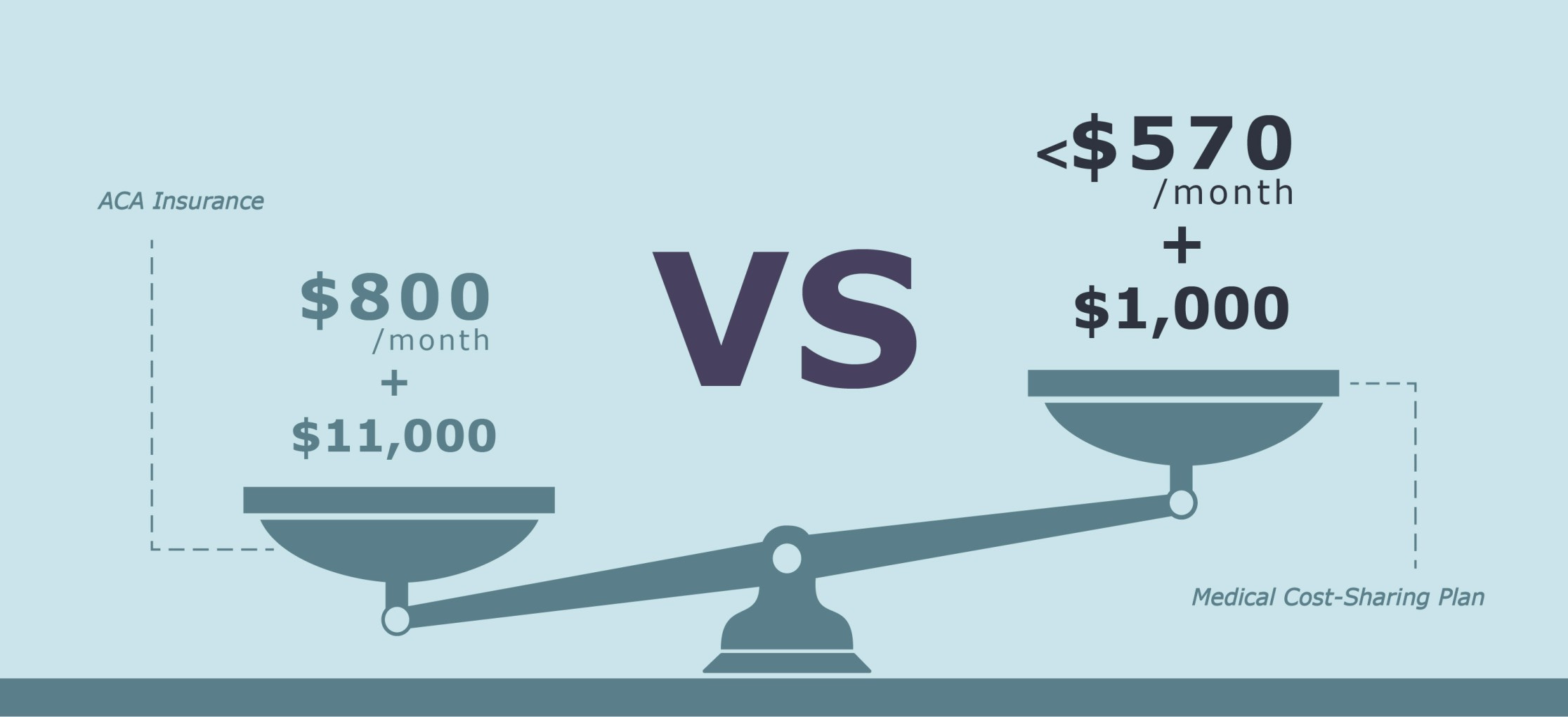

…a much better deal for a family plan

Fortunately, some pre-ex sicknesses are exempt from this waiting period if well-controlled: high cholesterol, high blood pressure and diabetes. We can discuss your situation during your education process. Those who can afford to can get ObamaCare AND Sharing, dropping insurance after the pre-ex period has expired. After all, why would a sane person want to keep a policy that excludes half a region’s providers, exposes one to such high out of pocket, or fights against claims

Whether with Sharing, ObamaCare or Medicare, another account I offer was featured in Forbes as something a bit different than an HSA. It doubles in value over 3 years and serves as a “supplement” policy that’s great for Out of Pocket costs like dental, mental, braces, electives, ongoing chronic therapies or maintenance meds, procedures, tests, labs and chiropractic.

As RFK adviser Callie Means explained here, ObamaCare incents over-utilization and excessive charges. To avoid getting booted by the insurer out of its network, doctors are too afraid to think outside the box for the hard-to-treat chronic diseases now saddling 50% of Americans. It’s a matter of life or death to get out of insurance.

To just connect with me to discuss benefits or Health Freedom, do so at LinkedIn and message me there.

Or subscribe to my weekly Freedom Hub health zooms, noon ET Wed & Thursday’s. Weekly I platform entrepreneurs and experts solving problems (and exposing the truth) - and making a better world that eases life for all of us.