CEO's tragedy leads to attack on Insurance, and millions leaving for Sharing

Upgrading from claims-denying ObamaCare to choice-enhancing Medical Cost Sharing seems equivalent to leaving a Bank for a Credit Union

Credit Union members love their affordability and compassion, same with members of Medical Cost Sharing communities. Sharing plans costs HALF what insurance charges, minus any taxpayer subsidy, and don’t handcuff choices via networks that exclude the best doctors and hospitals a patient would want if suffering heart disease or cancer. Do you think you’re covered if you belong to an insurance network?

Hey Pot - Your Kettle is Black Too

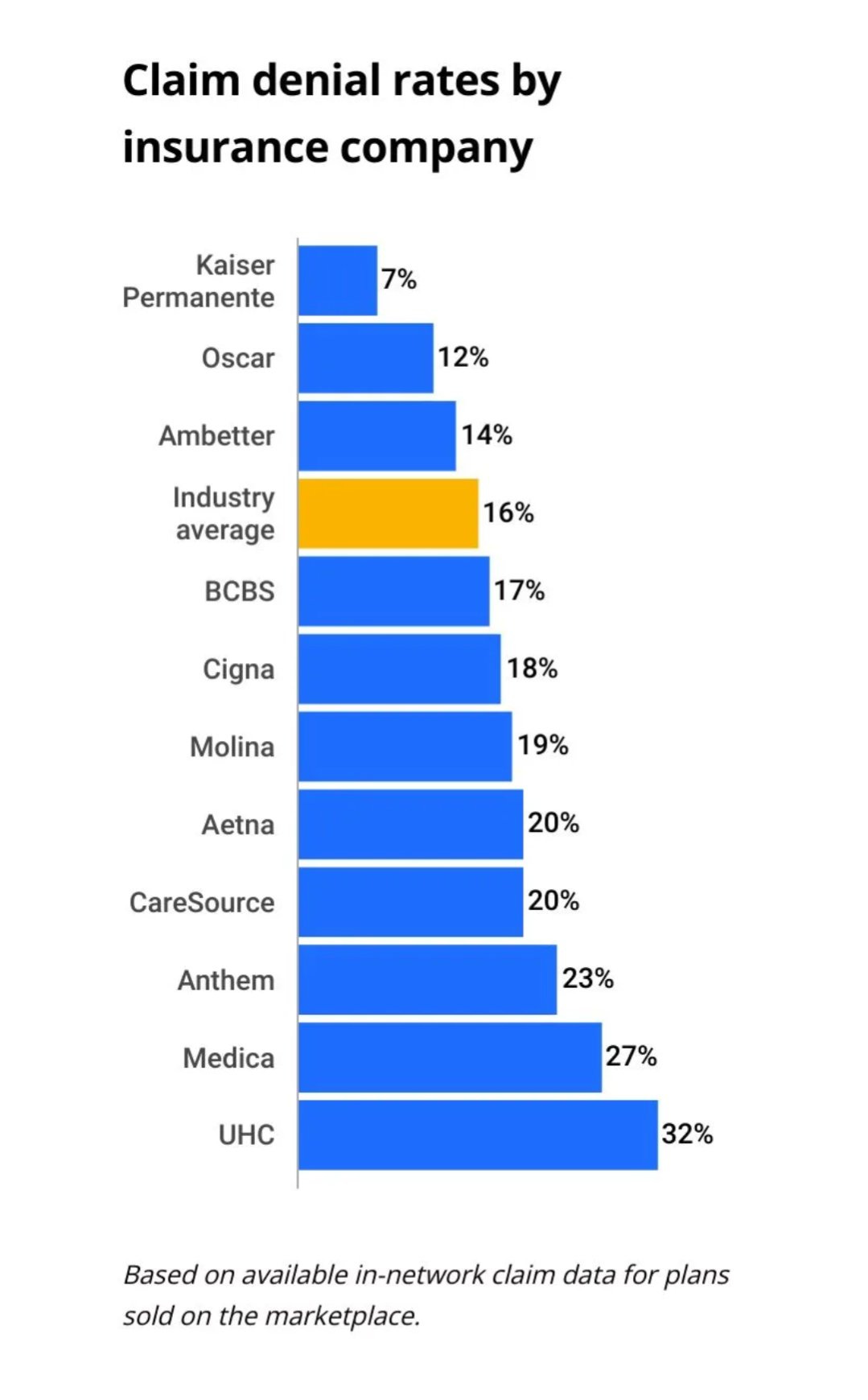

Yet the media during Open Enrollment lies every year that only Sharing doesn’t guarantee claims. Insurers do too - in the fine print, e.g. “Prior authorization approval does not guarantee that a health insurance company will cover the cost of care…”. And with the anger over Insurance claims denials instead of sympathy for the murdered CEO of the largest insurer, we need both sympathy for the family but also an honest conversation over insurer abuse of Americans.

I’m a Cash Patient - End of Story

This is because the media is claiming now that insurance networks are good, warning hospitals might exclude a member of a Sharing community. This is true, but then again our Forbes-featured brokerage advises our members not to tell the provider of their membership in a Sharing community. All a Sharing member needs to tell a doctor is, “I’m a cash patient. Do you have a discount”? Whether our Sharing Community helps the member pay bills is none of the provider’s business.

After all, if you’re getting help from GoFundMe or a Rich Uncle, or a Sharing Community, what difference should it make to the payee how you got your money - as long as the bill gets paid? When hospitals find out a patient belongs to a Sharing Community, cynically the hospital might try to deny the affordable cash price to the patient. That’s why we advise patient just to tell providers they are a cash patient.

Your Role in Creating a Cash Market

It’s even a beneficial political act to become a cash patient, because with passage in Trump’s first time of a rule for hospitals to disclose their prices, it’s only with patients working with our Concierge on locating quality-priced providers that we ever can hope to have a market with reasonable health prices. With current opaque pricing, health benefit costs rise annually in the high single digits - that is unsustainbable. Hospitals are resisting disclosing their prices, so Americans need to step up to help our brokerage demand price transparency. You can do this by sharing this article with family and business-owning friends, to contact me at the link and QR code in the image farther down this article.

Bankrupted from Out-of-Network Surprise Bills

Upgrading from ObamaCare to Sharing is critical for patient finances and peace of mind. That’s because nothing is worse than being hospitalized to discover that one of your providers is charging full price because they’re excluded from ones insurance network. Despite a federal limit on surprise, out-of-network bills for emergency services, medical bankruptcies still happen - because of networks, forced by Obamacare.

When acting as a cash patient as a member of a Sharing Community, you pay for a sickness or accident only the first few hundred (or thousand) dollars - depending on the Out of Pocket (OOP) risk you accept (in order to drive down the monthly Sharing Community membership charge). Above that “deductible” - what we phrase as the “Initial Unshareable Amount” (IUA), the Sharing Community pays for everything. (Just be sure to call our Concierge just as soon as you triage any emergency, to ensure bills get paid and you have advice on medical options).

Best Retirement NestEgg

And for the IUA our healthplan includes the tax-advantaged Health Savings Account (HSA), an easy way to roll over $3600 annually ($7K/family) until one has a $100K nestegg (or more) for retirement - when patients NEED such help for Out of Pocket costs for dental, Medicare gaps and long term care. If retirement doesn’t bring medical OOP, use HSA funds for non-health expenses, like vacations or local activities.

The Better Account for Out of Pocket

Those with ongoing (chronic) expenses or regular therapy - or patients needing lots of money for an expensive surgery or kids’ braces (or retirees facing Medicare max OOP limits of $13K (or higher with prescriptions) - may want to buy another account that doubles in value over 3 years. Watch the video then click “enroll” for, say, the $85/month option, doubling the value to $5K for OOP (with higher monthly charges to double to $10K, $15K or even $25K). This makes my best recommendation for dental, urgent care, chiropractor and ongoing therapies - just make sure your provider agrees to bill the account company directly, as opposed to making you pay and then you file for reimbursement.

Not just Families, but also Business Owners

Not only can families get more affordable major medical protection without losing choice of provider, but also business owners can get out of the risk business by replacing their group plan with Medical Cost Sharing - under an arrangment called a “ListBill”. For a quote, just fill in a “census” of employees and “listbill agreement”. The boss can pay everyone’s monthly Share amount or deduct all or a portion of is from payroll - perhaps in the latter case making workers whole with a broad bonus payment.

ObamaCare’s Premium Subsidy Tease

Sharing’s affordability does stem from waiting periods for conditions that pre-exist enrollment, but that’s a problem only for the couple years our members have to wait before protection kicks in for pre-ex. Those with sufficient funds sometimes double dip, buying Sharing AND an exchange plan - the latter only for the duration of the pre-ex phase in (dropping ObamaCare after a year or two). Lower income exchange enrollees can qualify for a premium subsidy - but beware if you earn more than you predict, or such subsidy will be clawed back when filing taxes. In this case the subsidy becomes a tease. Those working for companies that offer Sharing might elect instead to purchase an ObamaCare plan, if too sick to risk the pre-ex phase in; or those workers too might want to buy both the Sharing AND exchange plan for just this two year phase in period, dropping insurance once this period ends.

Democrats Don’t like ObamaCare Alternatives

Beware the attack on Sharing from state Insurance Commissioners and some Democrats who don’t want the competition with their ObamaCare exchange programs - or even dreams of foisting Medicare on all of the country. Some of the commisioner heat is justified, as shysters infect the Sharing market just as Insurers face corruption, like the cynical use by insurers of Artificial Intelligence to arbitrarily deny claims - or by the outrageously high percentage of denials by the company whose CEO was shot.

Sharing Important for Spouses and the Working Poor

Spouses, too, will want Sharing to remain as an option, as expensive specialty drugs force large employer plans to “carve out” coverage for spouses. Protecting Sharing will matter to poor folks with some money, when unsafe amounts of government debt require belt-tightening that throws some Medicaid eligibles onto the market. Those losing Medicaid might gain a low-cost exchange plan, but remember the above warning how better earnings than predicted could result in an IRS retaking of such subsidy - in which case Sharing makes a better value if losing Medicaid.

Network Providers Even Can Become Dangerous

Sharing’s openness to any provider (since all of them offer cash prices for cash patients) becomes important when hospitals or providers on an ObamaCare patient’s network are low-rated, or happen to be pHARMa simps who bully patients with independent views (such as, perhaps, following the brilliant advice of Dr. Mercola or incoming HHS Secretary RFK, or other frontline heroes censored during the Plandemic tyranny). Beware doctors compromised themselves over fear of being booted from the insurance company’s network. Only membership in a Sharing community offers patients an escape from network-damaged doctors.

Use Open Enrollment to Escape ObamaCare Networks

In the face of an expensive, cruel cartel (that is Healthcare), independence is key. Use our brokerage to become a cash patient; access the system via discounts, not memberhip in a hostile network. View my Image above and click the link or QR Code, to watch the video and fill in the questionnaire whose answers will be emailed to me - at which point I’ll invite a conversation to learn more about what you seek and whether we can help.

P.S. To learn more about health innovation, subscribe for my weekly Biz & Politics zoom noon ET on Wednesday.