It’s just business. Special Interests seek control of markets not just from offering quality goods and services (the “economic means” as written by the fierce social critic Albert Jay Nock), but also from contributing re-election financing to chairmen of congressional committees and buying advertising on mainstream media (Nock’s “political means”). Health insurers are no different.

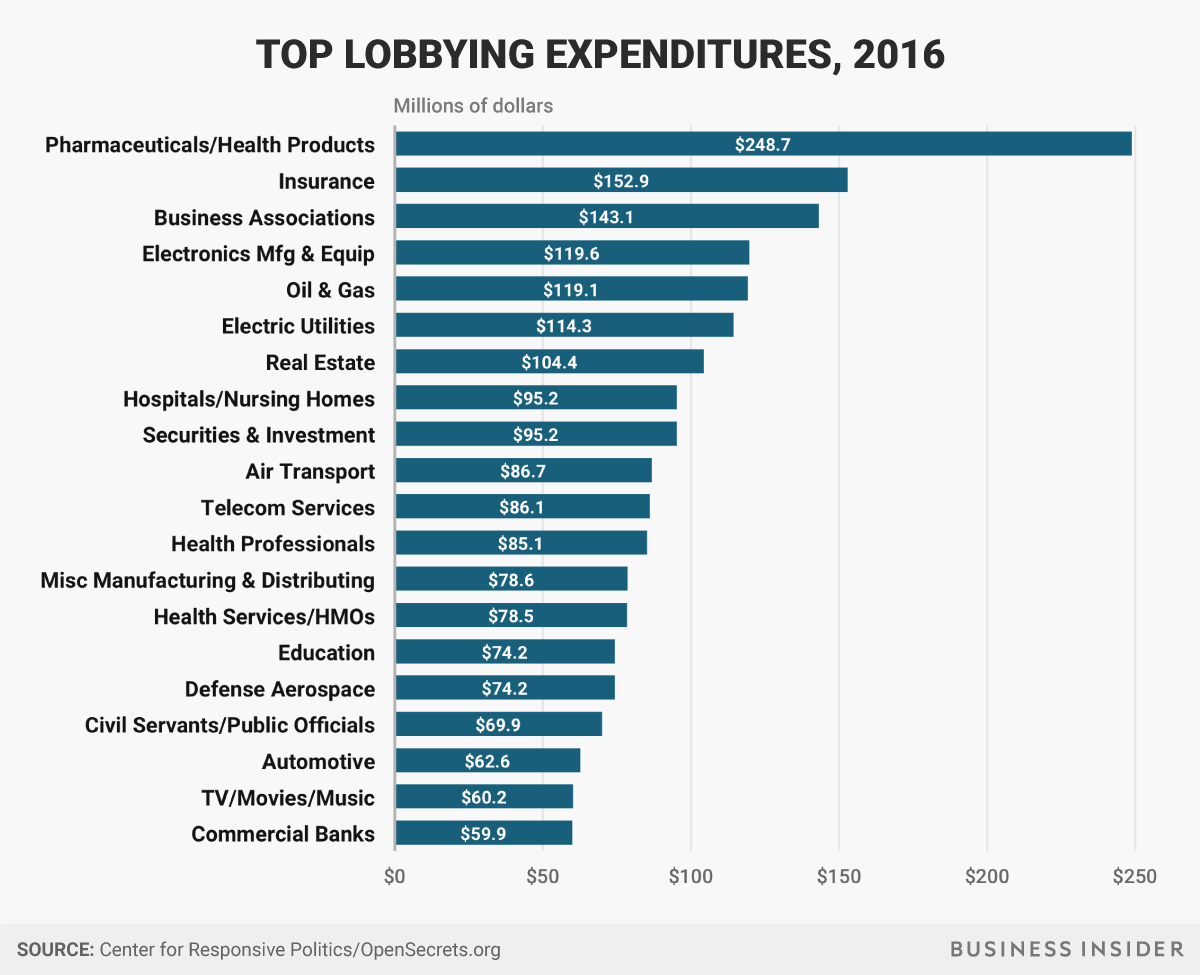

They’ve spent more on lobbying than any special interest apart from pharma - way more than energy (think oil). And like any other business investment, giant health behemoths expect a return on investment. So when Medical Cost Sharing companies exploded in response to ObamaCare as a threat to BUCAH (Blue Cross, United, Cigna, Aetna and Humana) - as credit unions threaten market share of banks - the larger incumbents will expect their political and journalist friends to discredit the competition. The story need not be fair.

(Even this chart understates health payer lobbying: look how they separated HMOs and moved them down the list).

The discrediting started with a scapegoat, Aliera, moved onto a few small Sharing outfits and currently is targeting a big Sharing company - Liberty. None of them are without fault, perhaps, and critics claim they’re unregulated. But that’s not completely true. Sharing isn’t insurance, so it’s not regulated by insurance regulators. But if a Sharing company commits fraud, they risk prosecution by state Attorneys General. And one of the above companies was shut down by the govt - that doesn’t sound like a lack of regulation.

Darren Fogarty wrote a great defense of Sharing against previous media attacks, here.

But regulation by government, people should know, doesn’t guarantee safety or quality. As will be discussed below, insurers are regulated, but these regulated entities denied almost 30% of claims in one state. Regulations make a poor substitute for caveat emptor (careful shopping) and the service of the courts as adjudicators of disputes. Indeed, the National Health Federation has a campaign for entrepreneurs to escape smothering red tape if they follow registered certifying organizations - a legislative fix that would replace the moral hazard of trusting regulation to protect consumers with a dynamic system that would incentivize consumers and suppliers to keep improving quality.

In a new industry mistakes are made, such as not assuring understanding by the customer on the differences between insurance and Sharing. But in some cases the customer just got bit by the pre-existing clause they DID understand but just hoped wouldn’t manifest. It’s bad for business to have unhappy customers - indeed, Hazlitt in his iconic classic, “Economics in One Lesson”, warned loss of reputation served as the most powerful “regulation” of all. Agents constantly hone their pitch with customers to ensure they’re a good fit for Sharing. No one wants unhappy customers; it’s bad for business.

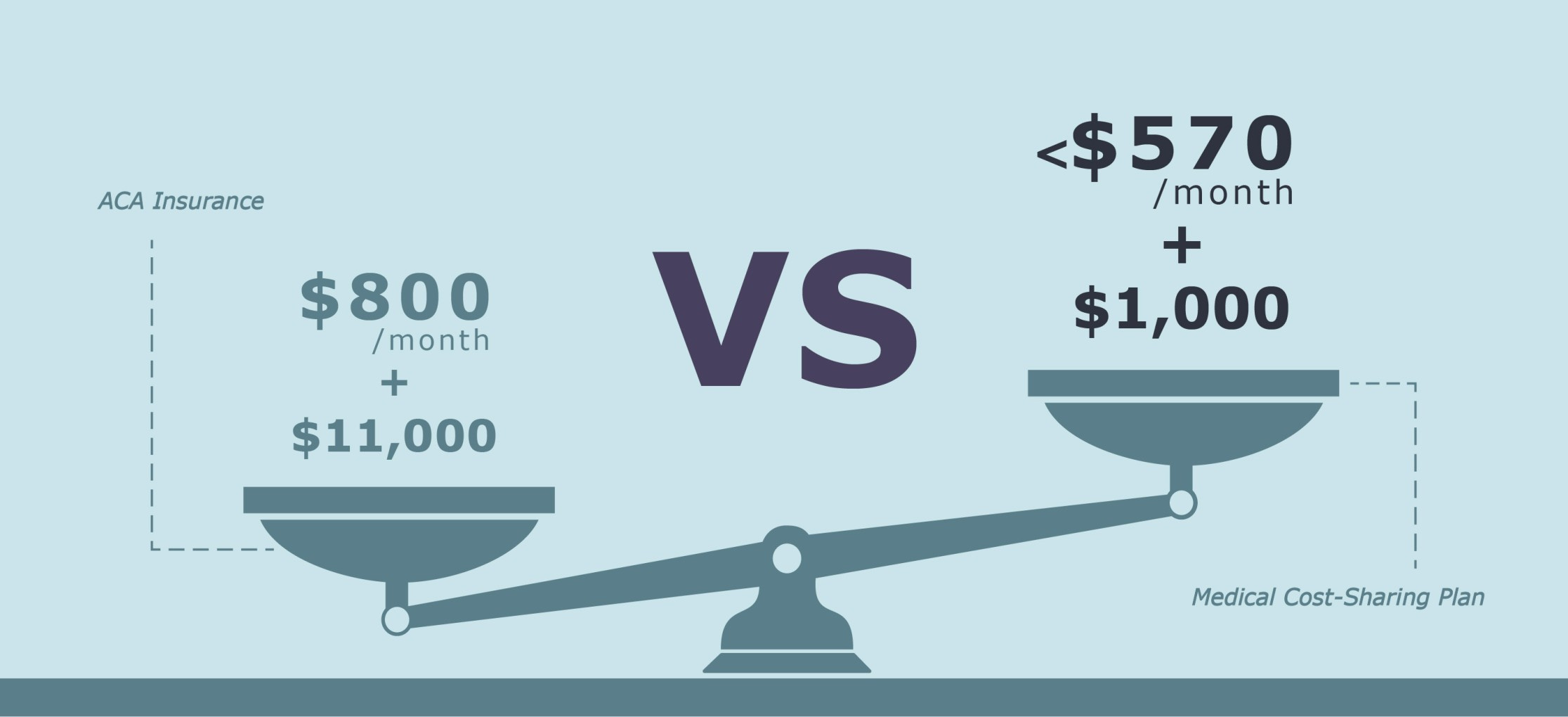

Sharing is different, and customers need to embrace the upgrade. It definitely has advantages over insurance - which costs too much and restricts choices dangerously. Insurance costs too much because they’re underwriting people who were sick before enrolling, something most insurers of other lines - and Sharing - won’t do (Insurance won’t cover a home after the fire, for example).

While good for those with cancer, heart disease, diabetes or other chronic conditions, the “guaranteed issue” nature of insurance comes with outrageous, monthly premiums - which lead to political calls for taxpayer subsidies which exacerbate the national debt, imposing burdens on our future generations. Sharing, on the other hand, can charge monthly as little as $250 per person, or $550/family, while fixing the healthcare cartel from its enabling of price-sensitive shopping.

And if one suffers a catastrophe and spends the average $6,000 deductible required before the Insurance kicks in, he discovers a likely surprise bill from the facility, surgeon or anesthesiologist excluded from the NETWORK. Most Sharing communities don’t handcuff choices via networks - and thus have little reason to expect surprise charges.

What makes reporters’ attacks on Sharing unfair is their tendency not to expose similar problems with insurance. It takes licensed health agents like myself to blow the whistle that the “emperor has no clothes”. A few consumers may complain to state insurance departments that their Sharing company denied claims based on pre-existing condition guidelines, but insurers in California denied almost 30% of claims in one year.

Agents licensed to sell insurance are recommending families and businesses increasingly choose instead Sharing, because it can be a better deal for the customer. For those recently sick, it’s good to have a backstop - whether via ObamaCare, Medicaid or, prior to that, state risk pools. But to force everyone into insurance would stifle access to the best doctors who refuse inclusion in networks used by insurance.

Most important, the best doctors support the independence movement enabled by Sharing (See points 2 & 7). That’s because Sharing uses a Concierge to help patients shop prices for drugs, tests and specialists. Price-sensitive shopping is how America can allow a real market to exist in health. Sharing is saving health care from the special interests who want nothing but the status quo. Millions have left insurance and never will leave Sharing.

Any victim of misconduct deserves justice and support, but that goes for those misused by any entrepreneur in any market. The answer isn’t to over-regulate or outlaw the alternative to insurance. That would be like outlawing credit unions because of an isolated incidence of fraud that happens even more frequently with banks.

Any family or business owner frustrated with insurance that’s too expensive, adversarial with claims or choice-handcuffed via networks, is welcome to email me at HealthEmpowerment4U@gmail.com, to learn what the better Sharing companies are. Forbes featured how our brokerage combines Sharing with HSAs, with a Concierge to help patients shop on price and quality:

And if anyone wants to “do something” political about abused customers, let’s start with AAPS’ legislative recommendations (which focuses on problems that actually matter):

End regulations blocking alternatives to ACA, employment-based, Medicare, and Medicaid plans, while allowing those who wish to keep their current government plan to do so.

Encourage Price Transparency. Health care entities receiving taxpayer-subsidized funds from any source must disclose all prices that are accepted as payment in full for products and services furnished to individual consumers.

Decouple Social Security benefits from Medicare Part A. Citizens should be permitted to disenroll from Medicare Part A without forgoing Social Security payments. This would immediately decrease government spending and open the potential for a true insurance market for the over-65 population.

Repeal Medicaid rules that decrease Medicaid patients’ access to independent physicians. ACA requires physicians ordering and prescribing for Medicaid patients to be enrolled in Medicaid. This creates barriers for Medicaid patients who seek care from independent physicians but wish to use Medicaid benefits for prescriptions, diagnostics, and hospital fees. This is a particular problem for Medicaid patients seeking treatment for opioid addiction.

Explicitly define direct patient care (DPC) agreements as medical care (instead of insurance) so patients can use their HSAs, HRAs and FSAs for DPC.

Expand Health Savings Accounts (HSAs). (1) repeal the requirement that an individual making a tax deductible contribution to an HSA be covered by a high deductible health care plan; (2) allow members of a health care sharing ministry to participate in an HSA; (3) increase the maximum HSA contribution level; (4) allow Medicare eligible individuals to contribute to an HSA; (5) allow HSAs to be used to purchase health insurance; (5) fund HSAs through tax credits; (6) Roth-style HSAs.

End Restrictions on Health Sharing Ministries. Open the door for secular charitable sharing plans. Health Care Sharing Plans engage in voluntary sharing and are not a contractual transfer of risk.

End Tax Discrimination. Individual’s payments for premiums and medical care should not be taxed differently than payments made by employers.

Encourage indemnity insurance instead of plans with limited networks of physicians and facilities.

Increase options for addressing pre-existing conditions. Invigoration of competition, by implementing the above changes, would bring a variety of products for patients with pre-existing conditions and most importantly lower overall cost of care.

God bless AAPS, the choice-respecting alternative to the corrupt AMA.

Back to Sharing, one thing we’ve learned via Covid is that self-thinking Americans cannot rely on a corrupt press or political system to provide trustworthy information. Caveat Emptor teaches buyers to undertake care in their choices, including their sources of information - including whether to buy insurance out of manufactured fear of Sharing.

Charles,

This is an excellent review of the current situation in the USA. In fact, when you add all of the healthcare based lobbying expenditures is exceeds $659 million! That is a lot of influence to be paid back. Sharing is essentially a mutually beneficial group of people. Mutual associations are historic and, before Big Govt, the best way for people to solve problems and help those in need. Of course, Churches did their part too!

Medical Cost sharing is a way back to bedrock American values of cooperation at the most local of levels. There is a place in the US for Medical Cost Sharing.

A couple of points. Carriers are generally protected by guaranty funds. Cost sharers and self insured plans are not except as creditors in general bankruptcy. Just understand that is a difference. As to cost and value no employer should use traditional self insurance with leaky stop loss much less buy a group plan. The author supports ICHRA a bailout Trump gave big employers to cheaply comply with ACA. They use this approach to fund a HRA and make available health purchase options.

A better method is to use this same approach but have the emp0loyer self insure and then fund using cost sharing and ACA plans as needed. Some health shares have a phase in that will permit the employee coverage for excluded condition until coverage is permitted. The employer bus ACA plan for cat coverage and pays a second premium to the cost share. When a house is on fire who cares the cost of water?

The employer then provides a TPA who administers the plan and the employer takes a small sliver of capitated risk to top off teh benefit provided to each employee. For any employer that must provide competitive benefits or simply wants to for moral reasons this approach is the best. For those employers seeking to comply with ACA then the pure unadulterated ICHRA is the most economical.